The UK Government response to COVID-19

The UK healthcare system is public and therefore completely subsidized by the taxpayer. What does that mean exactly? Despite the obvious positives (ie: free healthcare!), having a fully public healthcare system means that space and beds are limited, patient waiting times are long and organizational change is extremely slow.

Public sector pressures have given rise to the private healthcare system in the UK.

Increasingly, people are demanding a better, smoother experience with their healthcare provider: out of office visiting hours, delivered prescriptions, shorter waiting times etc. A great example of these shifting market dynamics is Babylon, the British poster child for healthcare tech. Babylon is effectively replacing physical NHS clinics with its private-sector solution. After the opening of Babylon’s London clinic, an enormous influx of patients followed. The clinic attracted 10x more patients than the NHS clinic it replaced.

Then came COVID-19. Suddenly, the NHS found itself under the additional pressure of a global and unprecedented pandemic. The necessity to adapt has placed immense pressure on the UK healthcare system and in turn, led to the emergence of new – and lasting – trends.

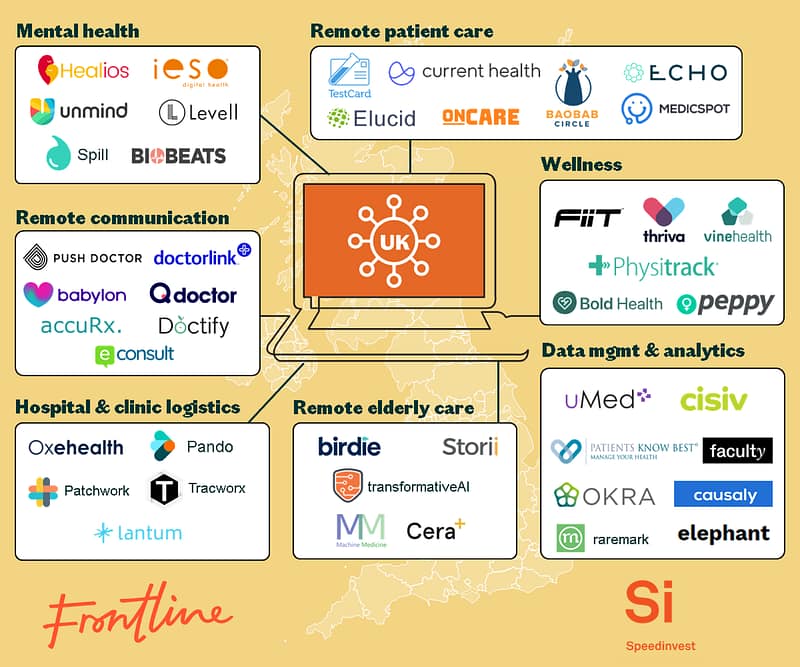

Remote communication

REMOTE ELDERLY CARE

There is a strong possibility that lockdown will be extended for the 11.4m elderly in the UK.

This population segment is likely to need physical therapy as well as help completing everyday tasks, which means services that match carers/patients could be essential (ex:Cera or Birdie). IoT devices connected to software that track vitals/accidents could also prove important (ex: Current Health and Testcard).

In the longer term, consumer behavior may shift towards broader remote management of illnesses like diabetes, hypertension, heart conditions, Parkinson’s etc.

Hospital & Clinic Logistics

Between mid-March and mid-April, COVID-19 related admissions quadrupled, exposing the chronic shortage of hospital beds in the UK. A shortage of staff, equipment and a general lack of organisation in hospitals and clinics limit efficiency.

Workflow management tools that track beds, tasks and patients create visibility and accountability across staff to optimise patient flow. For ex: Frontline portfolio company, Tracworx, a wifi-based patient tracking system that allows hospitals to collect real-time data and generate reports on patient journeys throughout their facilities, to optimize efficiencies and improve standards of care. Founded in Limerick (IRE), Tracworx has expanded operations into the UK and has plans to expand further into the European market in the near future.

Side note: Tracworx has recently launched a Covid-19 specific solution to assist hospitals and clinics geared at assisting with social distancing efforts and the tracing back of movements to identify potential patterns and hotspots.

Back in the “normal world” companies like Pando and Patchwork are introducing flexible work hours and logistics management. Let’s imagine a world where this is the new norm. Task trackers could change the way healthcare practitioners get paid-from hourly rates to a reward based system, resulting in a better incentivized workforce.

Data Management & Analytics

When the Prime Minister initially suggested a herd immunity response to COVID-19, the government flirted with the idea of working with Faculty and Palantir to estimate the spread of the virus. In theory, location and location data could also be used to estimate hospital staff and equipment demand.

Other useful data sources include: medical records, research reports and patient symptom data (ie: through communities like Raremark). NLP based software could potentially assist doctors in making more accurate diagnoses and prioritizing the right patients through the funnel (ie: sophisticated triaging).

It’s important to note that despite there being a wealth of healthcare data to analyze, information is not useful unless it’s centralized, sharable and secure. Therefore, next-generation data management software for clinicians and hospital staff could prove critical in enhancing the efficiency of the healthcare system. Examples include Umed and Patients Know Best.

Mental Health & Wellness

Since the outbreak, the NHS has launched a mental health hotline for its 1.4m staff. Studies show that depression and anxiety have spiked by 20% since lockdown as people cope with the loss of relatives, financial instability and isolation. Approximately 20k people have died since early May from Covid and 2m workers have lost their jobs-twice that of the 2008 crisis. As a result, mental health startups matching patients/therapists digitally are likely to gain traction. For example: Ieso, Unmind.

About

About Frontline

Frontline is the venture firm for globally ambitious B2B businesses on both sides of the Atlantic.

Frontline Seed strengthens and speeds up ideas at inception across Europe. Frontline Growth is a go-to-market first, capital-second fund, for fast and frictionless US-to-Europe expansion

Frontline has backed 60+ B2B entrepreneurs across Europe and the US, and has had numerous successful exits. Most recently: Pointy – acquired by Google (GOOGL) and Logentries acquired by Rapid7 (RPD).

Today, Frontline has $200 million funds under management, with offices in London, Dublin and San Francisco.

The firm is managed by partners Shay Garvey, Will Prendergast, William McQuillan, and Stephen McIntyre.

About Speedinvest

Speedinvest is a European venture capital fund with €400M+ AUM and more than 40 investment professionals working from Berlin, London, Munich, Paris, Vienna and San Francisco.

Employing a sector-focused investment structure, we fund innovative early-stage technology startups in the areas of Fintech, Digital Health, Consumer Tech, Network Effects, Deep Tech and Industrial Tech.

Speedinvest actively deploys its global network and dedicated team of more than 20, in-house operational experts to support our 150+ portfolio companies, including with US market expansion. Learn more: www.speedinvest.com

Sources:

- https://www.wired.co.uk/article/babylon-health-nhs

- https://www.nhsforsale.info/private-providers/babylon-new/

- https://www.theguardian.com/world/2020/mar/06/gps-told-to-switch-to-remote-consultations-to-combat-COVID-19>

- https://www.bma.org.uk/advice-and-support/nhs-delivery-and-workforce/pressures

- https://www.theguardian.com/world/2020/apr/12/uk-government-using-confidential-patient-data-in-coronavirus-response

- https://pharmaceutical-journal.com/article/feature/non-adherence-medicines-weakest-link

- https://www.hsj.co.uk/coronavirus/COVID-19-hospital-admissions-flattening/7027364.article

- https://www.standard.co.uk/tech/natural-cycles-track-coronavirus-symptoms-temperature-a4399286.html

- https://www.telegraph.co.uk/business/2020/04/08/two-million-people-lose-jobs-record-plunge/